When an airplane experiences turbulence it can be unnerving if you’re not used to it. Still, the pilot and crew — after telling you to stay seated and fasten your seat belt as a safety measure — typically stay on course so you can reach your destination.

That’s a lesson for investors. One of the bitter truths of investing is that stocks and bonds don’t always go up. As we have seen in 2022, in fact, sometimes that selloff can be quite dramatic — and painful.

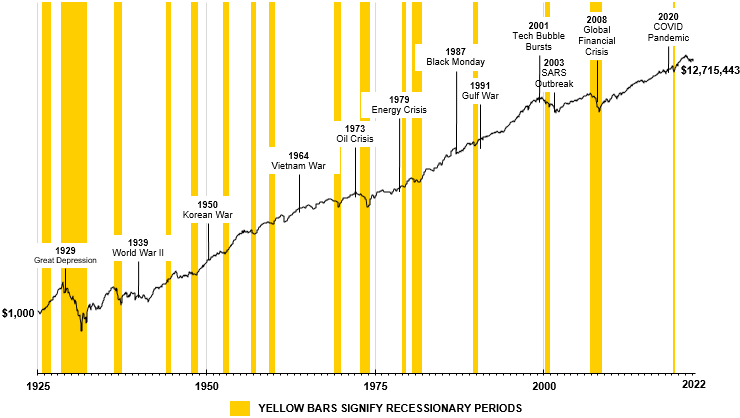

When facing bouts of market volatility, it is important to not focus on the day-to-day swings, but your longer-term investing goals. Of course, no one likes to see their hard-earned savings diminish, so investors often ask “How should I handle market volatility?" And “Should I sell stocks when markets are volatile?" That’s why it can be so hard to accept that often the best course during market selloffs is: Do nothing.

When times are tough, we want to limit our losses. Even when things are going well, we wish we had invested more. We all fear missing out.

But when you’re investing, giving in to fear is often a losing strategy. More often than not, investors with this mindset tend to buy high and sell low as they invest more in a rising market and pull money out in a falling market.