KEY TAKEAWAYS

- Chasing performance, fear of missing out, and focusing on the negatives are three common mistakes many investors may make.

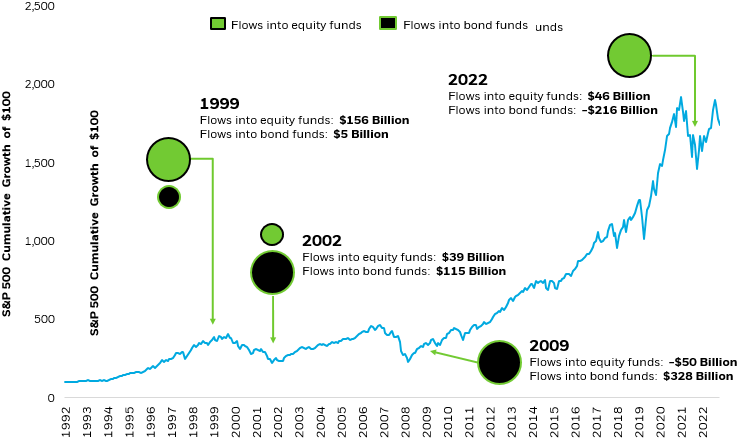

- History shows investors who overreact to near-term market events typically end up doing worse than if they stuck to their long-term plan.

- Just having an awareness of these typical pitfalls may help improve your portfolio’s performance.

Nobody’s perfect, especially when it comes to investing. One reason even the best investors may fail to keep pace with the broader market is because we’re only human, born to make mistakes.

In our daily lives, we know it’s hard to break bad habits, like eating too much junk food. The same is true for investing. Just as understanding which foods are better for you, knowledge is power when it comes to your portfolio.

So here are three common mistakes investors make — and some tips for how to address them.